Measure Now Before Budget Conference Committee

In what would be the largest change in retirement law surrounding cost-of-living benefits in nearly 30 years, the House of Representatives has passed a COLA Reform initiative within the Fiscal Year 27 state budget.

The initiative, passed by the House in late April, is based on the recommendations of the Special COLA Commission on which Association President Frank Valeri served as an appointee of Governor Maura Healey. It was Mass Retirees that called for the creation of the Commission, with the goal of not only improving benefits, but also developing a new way of funding future COLA increases.

Following the release of the Commission’s report in late December, our Association crafted a legislative proposal based on the recommendations contained in the report (see April Voice). With the detailed analysis of the Commission serving as a firm foundation, Association leaders presented our COLA Reform initiative to House leaders in March.

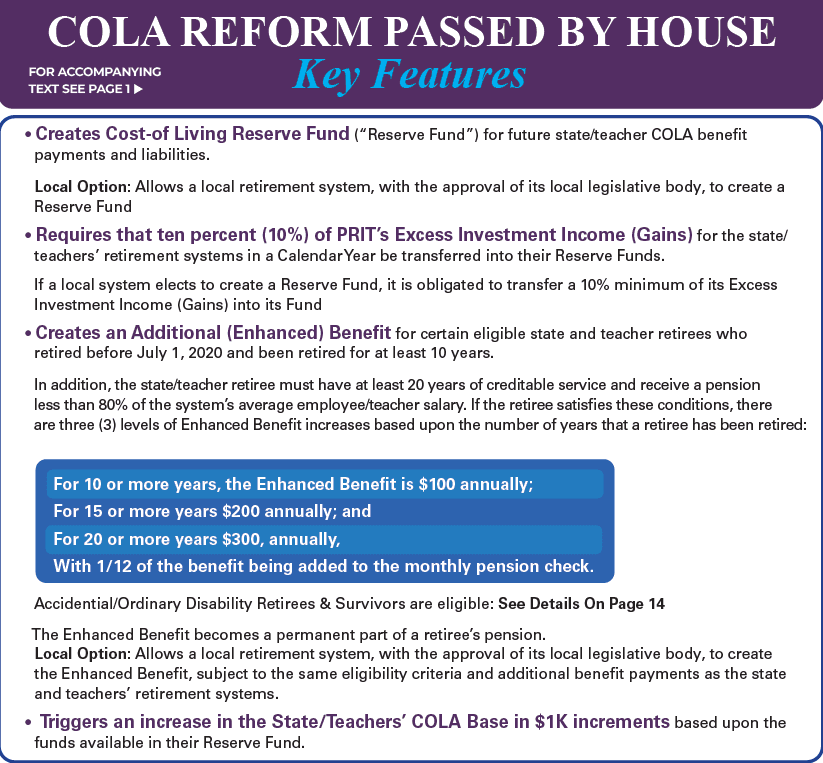

Central to the COLA Reform initiative presented by Mass Retirees, as well as the proposal passed by the House, are two primary concepts: The creation of a new Enhanced COLA benefit and the establishment of a COLA Reserve Fund.

“For several years we have been working to create a new COLA benefit to help career public employees who have been retired longer than 10 years. As a result of high inflation and rising health insurance costs, these retirees are having a hard time making ends meet,” explains Valeri. “Given the high inflationary period retirees have faced since 2021, the need for improved COLA benefits have never been in doubt. The high hurdle to overcome has always been the cost of improved COLA benefits and how to pay for it within the Commonwealth’s pension funding schedule.

“In addition to focusing on help for long-term retirees, a primary task of the Commission was to develop a new method to pay for improved COLA benefits – whether it be an Enhanced COLA or increasing the traditional COLA base. Through the work of the Commission and the actuarial staff of the Public Employee Retirement Administration Commission (PERAC), I believe that we achieved both primary goals.”

COLA PROPOSAL IN HOUSE BUDGET

After reviewing our initiative and analyzing the Commission’s report, House leaders opted to include a COLA Reform measure within the FY27 budget proposed by the House Ways and Means Committee in mid- April. The measure was then passed by the House on April 30th. See Page 19 for a summary of its key features.

“Over more than a month’s time, we met and discussed the budget with House Speaker Ron Mariano, Majority Leader Mike Moran, Ways and Means Chairman Aaron Michlewitz, and Republican Leader Brad Jones. Our discussions with them proved invaluable, and we are extremely grateful that COLA reform was included in the Ways and Means budget proposal,” comments Legislative Chairman Tom Bonarrigo, who leads our advocacy efforts on Beacon Hill. “And, we also thank Public Service Committee Chairs Rep. Dan Ryan and Sen. Mike Brady for their participation in the Special Commission and as always, their continued support in improving retiree COLA benefits.

“The fact that this measure is moving forward now is due to the respect that House leaders have for public retirees and our Association. It is also a testament to the solid work done by the Commission and PERAC to create a viable funding mechanism that will pay for the increased benefits.”

Due to the timing of the budget process in 2026, with the Senate releasing its version of the FY27 budget just days after the House finished its work, there was not proper time for Senate leaders to vet the COLA Reform proposal passed by the House.

Differing versions of the budget, as well as major pieces of legislation, are a normal course of legislative discourse. The FY27 budget is now in conference committee, where three members of the House and three members of the Senate will negotiate a final unified version of the budget to be enacted and sent to Governor Healey.

“It’s understandable that the Senate did not have time to act prior to taking up the budget in mid-May. That said, we have had very productive meetings with the Senate leadership from both parties, including Senate Ways and Means Chairman Mike Rodrigues. As was the case with the House leadership, there seems to be a deep understanding amongst Senate leaders that retirees need help,” said Association CEO Shawn Duhamel. “We’re cautiously optimistic that COLA Reform will have the support of Senate leaders, survive conference committee, and become law in 2026.”

In addition to a series of in-depth meetings with legislative leaders from both parties, Association officials have also met with senior Healey Administration officials and directly with State Treasurer and Receiver General Deb Goldberg.

“Massachusetts retirees deserve financial security that reflects today’s economic realities. I support the House’s inclusion of an enhanced COLA proposal in the FY27 budget and the continued focus on supporting longtime state employees and teachers who have dedicated their careers to public service,” said Goldberg, who chairs both the PRIM Board and State Retirement Board.

COLA RESERVE FUND

A primary task assigned to the 9-member Special COLA Commission was to study and recommend a new funding source to pay for COLA improvements going forward.

Dating back to the first COLA law in the late 1960s, the main challenge in increasing benefits has been paying for the new benefit. As reported in our recent “History of the COLA” article, funding became even more of a hurdle following the establishment of modern pension funds in the 1980s, which ended pay-as-you-go pension funding policies across the country. This means that each unplanned increase in benefits must be both accounted for and funded within the system’s pension funding schedule.

Under the COLA Reform proposal passed by the House, 10% of annual excess investment gains (above the assumed annual rate of return, which is set at 7% for the State and Teachers’ Retirement Systems) will be earmarked to fund the Enhanced COLA and future increases in the traditional COLA base. While the COLA Reserve Fund does earmark a small portion of assets for the sole purpose of improved COLA benefits, the Fund itself is simply an accounting mechanism that does not change investment operations or policy. All assets will continue to be invested by the PRIM Board or the relevant local retirement system (through local acceptance).

The most important point to remember when it comes to this new policy is that it ensures that when the pension fund does well, that success will be shared directly with retirees through improved COLA benefits. This is a significant change in the state’s pension law, which previously rolled 100% of excess investment gains into the pension fund.

ENHANCED COLA FOR LONG-TERM RETIREES

Creating an Enhanced COLA benefit has also been a recent goal of our Association, as we frequently hear from long-term retirees struggling to make ends meet. The general concept that grew into the Enhanced COLA proposal was initiated by a conversation with former Boston Mayor Marty Walsh, during our Association’s advocacy work involving an increase in the City of Boston’s COLA base a decade ago.

The suggestion of then Mayor Walsh planted the seed with then newly elected Association President Valeri, who has focused on the creation of such a benefit ever since.

Using career public employment as a starting point, the Special Commission recommended the following criteria which is incorporated in the House proposal: A minimum of 20 years creditable service; retired for more than 10 years; receive a pension that is less than 80% of the average active employee salary for the system from which you are retired. Accidental and ordinary disability retirees are eligible regardless of years of service. Surviving spouses are also eligible, if their respective spouse would have met the eligibility criteria.

When establishing the eligibility criteria, the Commission recognized that most retirees with fewer than 20 years of creditable service have substantial private sector work history, qualifying them for larger Social Security benefits and, in many cases, private sector retirement benefits. Career public employees receive smaller Social Security benefits (if any) and rely more heavily on their public pension as a result.

To make sense of the pension criteria we are providing the following example: In 2024 the average State employee salary was $84,500 and Teacher salary $85,600. Therefore, retirees meeting the criteria with an annual pension of less than $67,600 and $68,480 respectively would be eligible for the Enhanced COLA. The earnings threshold will increase with the respective average salaries in each retirement system.

Under the proposal, the Enhanced COLA provides the additional annual benefit at three different thresholds. For details, see pg. 19 Key Features.

It is important to point out that, like the traditional COLA benefit, each Enhanced COLA benefit becomes a permanent part of a retiree’s pension. As we have previously reported, the cumulative nature of the COLA is a benefit secured by Mass Retirees in the mid-1970s and remains somewhat unique to Massachusetts. In most other jurisdictions the COLA is treated as a fixed one-time bonus and is often capped at a few hundred dollars annually.

Under the language contained in the House’s proposal, the Enhanced COLA would take effect on January 1, 2027. As this is a new benefit with a unique eligibility criterion, implementation of the Enhanced COLA is going to take some time. This is similar to the delay in the implementation for the state’s Basic Life Insurance benefit, which was passed into law in 2024 but did not take effect until 2025. As with any new benefit, implementation challenges are to be expected.

As is the case with the COLA Reserve Fund, adoption of the new Enhanced COLA benefit is also local option.

COLA BASE FOR STATE AND TEACHERS’ RETIREMENT SYSTEMS

The one main difference in policy between the initiative developed between our Association and that proposed by the House is an increase in the COLA base for the State and Teachers’ Retirement Systems. Set at $13,000 since 2012, our initiative sought to increase the base to $16,000 starting in July 2026 (FY27).

To do so, the Commonwealth would have to upfront the $1.8 billion in unfunded liability and hundreds of millions in new annual costs carried by the new benefit level. Each $1,000 increase in the State/Teacher COLA base carries a price tag of $600 million in total liability – a cost similar to the total cost of the Enhanced COLA.

Given the costs involved, the House opted to focus on establishing the Enhanced COLA benefit as soon as possible – a benefit geared toward helping those most in need. For FY27, State and Teacher Retirees will receive a 3% COLA on the current $13,000 base.

However, the reform measure sets a new process for increasing the State/Teacher COLA base in $1,000 increments utilizing the COLA Reserve Fund. Once the Reserve contains sufficient funds to cover the full upfront cost of each incremental increase, the COLA base will be increased accordingly.

As contained in the appendix of the Special Commission’s report, had the Commonwealth dedicated 10% of excess gains toward the COLA starting in 2014, the Reserve Fund would have held a balance of more than $4 billion by 2024 – an amount sufficient to fund a $19,000 State/ Teacher COLA base in perpetuity.

At the local level, the COLA base has been set by a vote of the retirement system and the respective legislative body since 2010. The average local COLA base is now just over $17,000 with a number of systems approving increase for FY27 (see related story, pg. 9).

Like the State and Teachers’ Retirement Systems, the composite analysis provided by PERAC of the 102 local retirement systems demonstrates that 10% of excess investment gains dedicated to a COLA reserve fund from 2014-2024 represents the cost of a $7,000 increase in the average local COLA base during the same period.

“The funding progress of our 104 public retirement systems over the past 41 years has been extraordinary. Not accounting for 2025, which was another year of double-digit investment returns, a growing number of systems are at or quickly nearing fully funded status. It is about time that retirees are allowed to share in this success,” points out Valeri. “I want to take a moment to thank PERAC Executive Director Bill Keefe, who chaired the Special Commission, and his staff for the hard work they put into the report and recommendations. Especially, the proposal would not have come together without the input of Chief Actuary John Boorack and PERAC Assistant Deputy Director Patrick Charles.”

Duhamel adds, “We believe the COLA Reform measure passed by the House strikes the right balance between fiscal responsibility and putting these trust funds to work for retirees.

After all, these funds were created for the exclusive benefit of the public retirees who have paid into the retirement system and earned a reliable pension benefit.”